Earn and maximise your yields in DeFi with ease

The power of DeFi at your fingertips enabling you to access more while doing less

Audited by

2.1% APY

Earn on your WBTC

7.98% APY

Earn on your DAI

15.49% APY

Earn on your USDC

Know exactly where your crypto is going

Feel the magic of automating your money and yield.

Set and forget

Buy and sell crypto consistently with pre-scheduled swaps to smoothly navigate market volatility.

Set your crypto in motion

With a range of risk levels and reward types to chose from,

Dezy has something for everyone.

15+

ways to invest

6

supported assets

1

interface for DeFi

For advanced DeFi functions

strategy

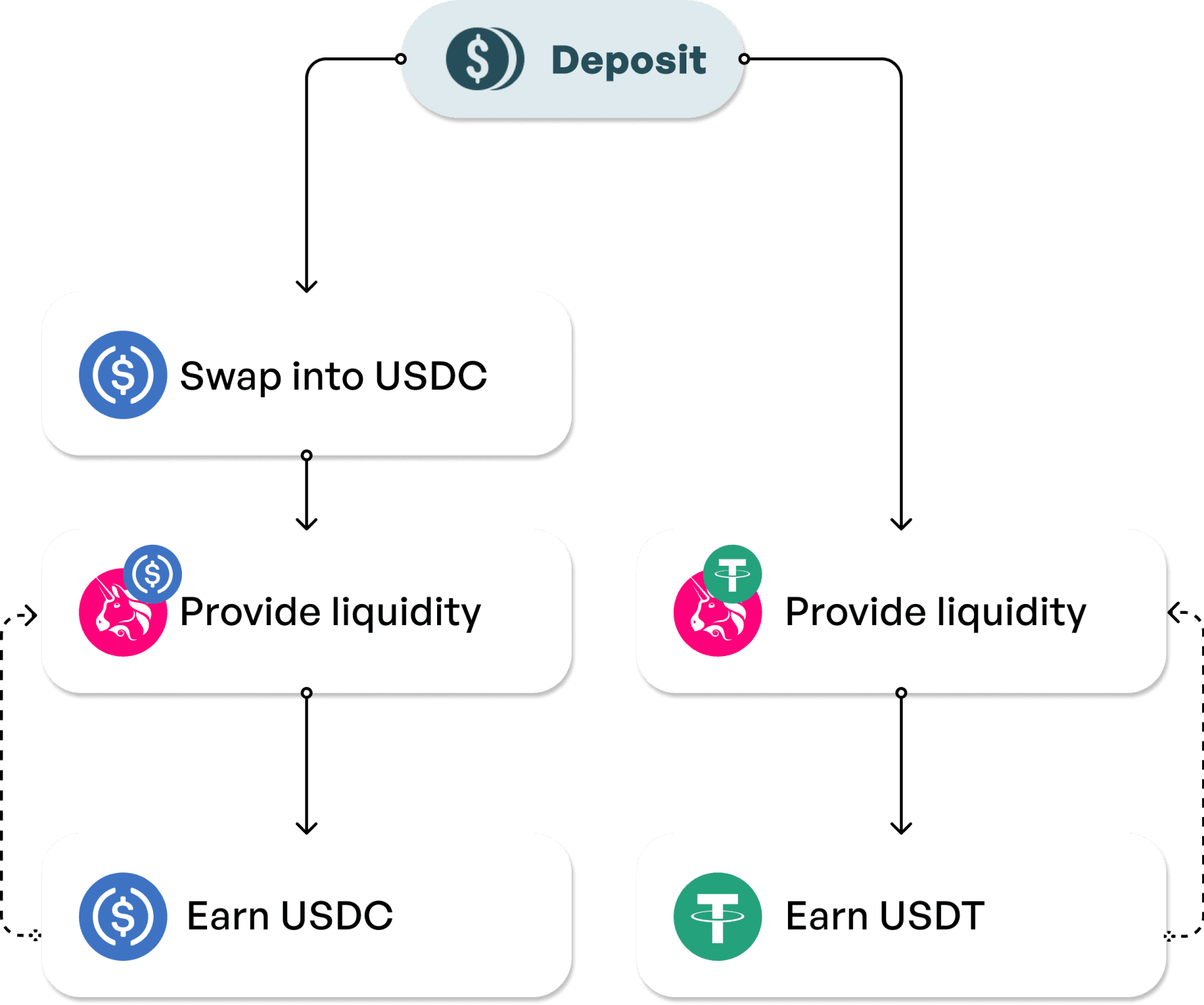

Create your own strategies and automate all your swaps, lending, borrowing across your favourite protocols. Even better, list your strategies and earn from sharing.

Made for you

For individuals

Find all the potential opportunities in DeFi in one glance, and get invested in them.

For DAO treasuries

Need more custom solutions for your DAO’s treasury needs? We’re here to help you figure it out.

Still deciding if we’re right for you?

These frequently asked questions might help.